Quantitative Python

Now that we have an understanding of risk

concepts such as the loss exceedance

curve,

value-at-risk, Bayes Rule, and

fitting distributions, we would like to have a

realiable, extensible and preferably open tool to perform these

computations. In the background, we have used a spreadsheet, which is

hard to extend. We have used GNU

Octave, which is good, but not a

proper programming language. Our favorite language at Fluid Attacks,Python, has modules for

statistics,

scientific computation and even

finance itself. Let’s take it for a

spin around this risky neighborhood.

Python has a whole ecosystem for numerical computing (v.g.Numpy) and data analysis

(Pandas) and is well on its way to

becoming a standard in Open

Science.

Being a free and open source tool, there are also many derived projects

which make life easier when coding, such as the Jupyter

Notebook, which allows us to selectively run code

snippets, much like in commercial packages such asMatlab andMathematica. This enables and

encourages, at least, initial exploration, although it might not be the

best fit for developing more involved code.

Let us see how we can automate the generation of a loss exceedance curve

(LEC) via Monte Carlo simulation. Here we will closely follow our

article on the subject, so as not to

duplicate information. In that article, we wanted to find a distribution

for losses based on expert estimations of occurrence likelihood and

confidence intervals for the impact:

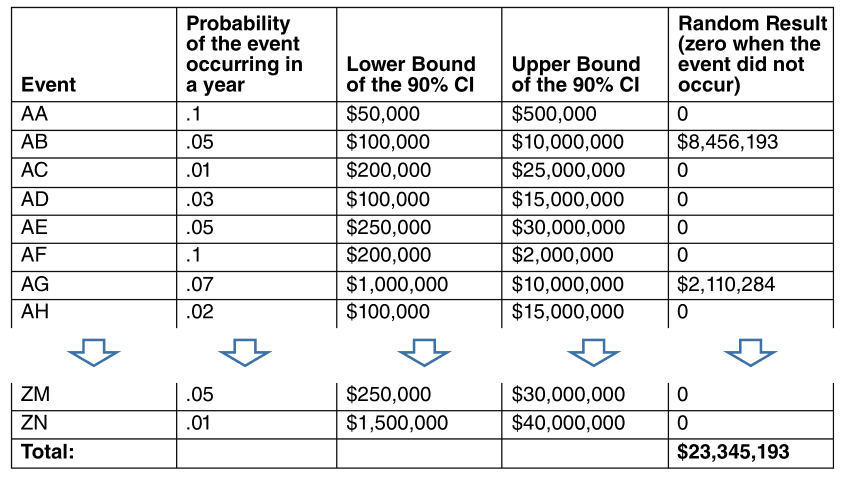

Figure 1. Table with input data.

So we need to read those values in our script. Since this is tabular

information of the kind that would be useful to view, say, in a

spreadsheet, it will be convenient to read this into a Pandas

dataframe:

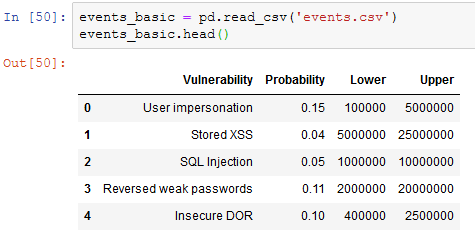

Importing pandas and reading data.

import pandas as pdevents_basic = pd.read_csv('events.csv')events_basic.head()

Figure 2. Data as imported into Jupyter like in our Monte Carlo

article.

We declare an event happens if a number taken at random is beyond a

certain threshold, given by the second column in the table above:

def event_happens(occurrence_probability): return np.random.rand() < occurrence_probabilityIf and when the event happens, we next need to know the extent of the

loss due to this single event. Recall that we modeled this with a

lognormal variable, whose parameters we got from the estimated

confidence interval:

def lognormal_event_result(lower, upper): mean = (np.log(upper) + np.log(lower))/2.0 stdv = (np.log(upper) - np.log(lower))/3.29 return np.random.lognormal(mean, stdv)All of the events in the above table can happen in a single year, so to

simulate a scenario, we need to find out, for each of them, if they

happen, and how much money they will cost us. Finally, we add all the

losses and return that single number as a summary of the losses in a

simulated year:

def simulate_scenario(events): total_loss = 0 for _, event in events.iterrows(): if event_happens(event['Probability']): total_loss += lognormal_event_result(event['Lower'],event['Upper']) return total_lossNow, the crucial step in Monte-Carlo simulation is to simulate many

scenarios and record those results. Let us write a function that does

just this, returning the results in a basic Python list, which we

could later turn, if we so wished, into a Pandas or Numpy-native

structure for statistical analysis. The function takes as input the

number of times we want to simulate scenarios:

def monte_carlo(events, rounds): list_losses = [] for i in range(rounds): loss_result = simulate_scenario(events) list_losses.append(loss_result) return list_lossesGoing graphic

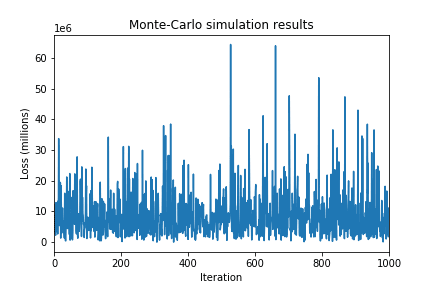

Just to get a feeling for the results, let us run a thousand scenarios

and plot them, that is, the result of each simulated year, in the order

in which they were obtained. As foretold, we could convert the results

into a Pandas DataSeries, if anything, to illustrate how they work.

We also need to import Matplotlib for

visualization:

import matplotlib.pyplot as pltresults = monte_carlo(events_basic, 1000)results_series = pd.Series(results)results_series.plot()

Figure 3. Raw Monte-Carlo results

It can be observed that the vast majority of them are in the fringe

between 0 and 15 million. But it is not infeasible to have results that

are way beyond the central interval. In order to rule out what’s simple

chance and what is really happening due to the distribution of loss, we

can simply run more scenarios. Tens or hundreds of thousands of

scenarios is a good rule of thumb, without sacrificing performance. A

thousand runs takes around 5 seconds, and 10000 takes around 50. At some

point adding more simulations does not necessarily improve the quality

of results. Your mileage may vary.

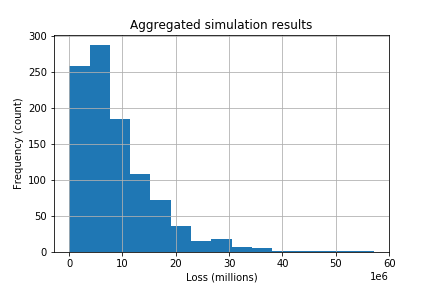

No matter the number of scenarios, the results are not as useful as they

could be until we aggregate them, v.g., in a histogram. Pandas also

provides a shorthand for this:

results_series.hist(bins = 15)

Figure 4. Histogram of results

We’re getting closer to the loss exceedance curve, but not there yet. We

can estimate probabilities simply by counting occurrences and

normalizing by dividing by the number of rounds and multiplying by 100.

Hence the estimated “probability” of a single value is the normalized

number of times that value appeared in the simulation. So let us take

evenly spaced values, and count the number of times each of those values

is exceeded (or matched). The numpy function cumsum does just

that, except in the opposite order: it adds the values seen up to a

moment. So if we take the intervals and the counts separately, revert

the counts list and then do cumsum on it, we get what we need, in

reverse order. To fix that we simply revert again:

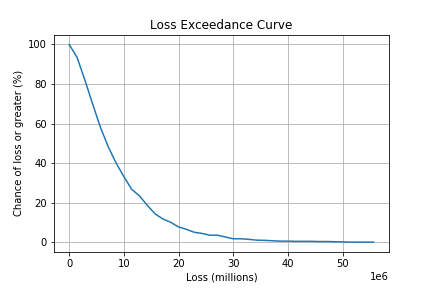

import numpy as npresult_nparray = np.array(results_list)hist, edges = np.histogram(results_nparray, bins = 40)cumrev = np.cumsum(hist[::-1])[::-1]*100/len(results_nparray)plt.plot(edges[:-1], cumrev)And voilà, we get our loss exceedance curve as we sought:

Figure 5. Simple loss exceedance curve like in our Monte Carlo

article.

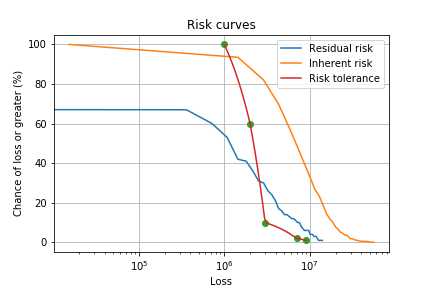

We can repeat the procedure with a more moderate dataset to obtain the

inherent risk LEC, in the sense that the probabilities and impact CIs

are lower. And finally, to obtain the risk tolerance curve, we give a

few points obtained from interviewing someone in charge, as described in

the original article and fitting a

curve to it using SciPy’s Interpolation

functions:

from scipy import interpolatexs = np.array([1,2,3,7,9])*(1e6)tols = np.array([100,60,10,2,1])xint = np.linspace(min(xs), max(xs))fit = interpolate.interp1d(xs, tols, kind='slinear')plt.plot(xint, fit(xint))All together in a single plot:

Figure 6. Loss exceedance curves like in our Monte Carlo

article.

Risk measures

Now obtaining the 5% value at risk is simply a matter of asking for the

95th percentile of the “distribution”, i.e., the actual

simulation results, in its Numpy-array incarnation:

>>> np.percentile(results_nparray, 95)23360441.53826834Hence the VaR, according to this particular simulation is a little

over $23 million. It is just as simple to obtain the tail value at

risk. If we had a mathematical function for the

distribution we would have to compute an integral in order to obtain it,

but since what we have is a discrete approximation to it, i.e., a

simple table of values, we can just average the values that are under

the VaR:

>>> np.average(results_nparray[results_nparray >= var])31949559.99328234Thus in case of a VaR breach, we can expect the loss to be of little

less than $32 million.

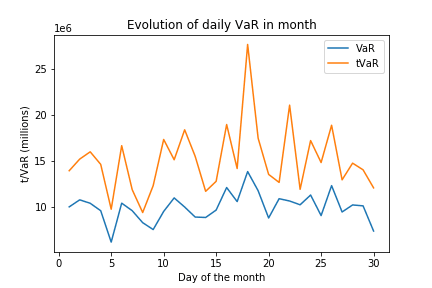

Let us simulate the input values for the simulation, as if we were

running the simulation every day with different occurrence probabilities

and impacts. Let us make up a DataFrame with random values for the

inputs:

def gen_random_events(): probability_column = np.random.random_sample(30)*0.1 lower_ci_column = np.random.random_sample(30)*(1e6) upper_ci_column = np.random.random_sample(30)*(9e6)+1e6 dicc = {'Probability' : probability_column, 'Lower' : lower_ci_column, 'Upper': upper_ci_column} events_rand = pd.DataFrame(dicc) return events_randNext we run Monte-Carlo on those, once for each day of a fictitious

month, compute the VaR and tVaR for each day and observe how they

evolve:

Figure 7. Fabricated VaR monitoring example like in our VaR

article.

Since this was a made-up example and the probabilities are sampled

simply, i.e., from a uniform distribution, the results are, well,

uniform. However for the sake of conclusion, we can imagine there is a

steady, if slow, trend towards raising the VaR. It is interesting that

the highest peak in tVaR corresponds to a VaR that is not that

different from its neighbors. This goes to show that one is not just a

simple function of the other, which is often the case in dealing with

uncertainty.

References

C. Davidson-Pilon (2019). Probabilistic Programming and Bayesian

Methods for

Hackers.C. Motiff (2019). Monte Carlo Simulation with

PythonB. Mikulski (2018). Monte Carlo simulation in

Python

Appendix: Full script

Download Python script or as Jupyter

notebook and input data for inherent

risk and residual risk.

*** This is a Security Bloggers Network syndicated blog from Fluid Attacks RSS Feed authored by Rafael Ballestas. Read the original post at: https://fluidattacks.com/blog/quantitative-python/