Kingmakers in Cybersecurity

Are you ready for a long yet full of insights article? If so, this is the piece for you, especially if you are in the world of cybersecurity and are developing your growth strategy to protect the world with your disruptive solution.

We are going to review in detail what are the forces that can drastically accelerate the success of a Cybersecurity vendor and position them as a leader in their sector.

Even if you (or your company) have created the most outstanding and disruptive technology or solution, growing in this market requires a deep understanding of the role that existing actors have.

I have already discussed in a previous article how relevant the choice of channel is when it comes to this market. Now, we will review the organizations that have the biggest impact and can transform a vendor into a king in their sector.

Understanding the role of the “kingmakers” is essential for any cybersecurity company aiming to scale effectively and become a leader, and through this article, we will be discussing who are the most influential ones for vendors that focus not only in business customers (B2B), but also for those that cater to consumers (B2C).

Buckle up!

Enterprise Cybersecurity Kingmakers

When it comes to those cybersecurity companies focusing on business customers, there are clearly at least four candidates for the title of Kingmaker: Global System Integrators (GSIs), Distributors, Cloud Marketplaces and Analyst Firms.

Each one of them has a different area of influence:

-

GSIs focus mostly on medium to large organizations,

-

Distributors have a higher reach to smaller and medium companies through their channel networks,

-

Cloud Marketplaces serve any size of organizations in different ways, and some of them are particularly well-suited for Managed Services Providers,

-

Analyst Firms, especially the most relevant ones, cater predominantly to large enterprises, yet their market evaluations and reports shape perceptions across the entire cybersecurity landscape.

Let’s discuss the role and impact of each one of them below.

Global System Integrators (GSIs)

GSIs such as Accenture, Deloitte, or PwC deliver sophisticated integration services that align with complex IT environments and high-level security requirements, being instrumental in embedding cybersecurity solutions within large-scale digital transformation projects.

Their extensive client networks and integration capabilities make them vital channels for vendors seeking enterprise adoption.

Finding out exactly how much revenue they make in cybersecurity products isn’t easy as it is not publicly available information. Estimates place that in the tens of billions (USD), reflecting the footprint they have in the market as well as the demand from their customers for integrated cybersecurity services.

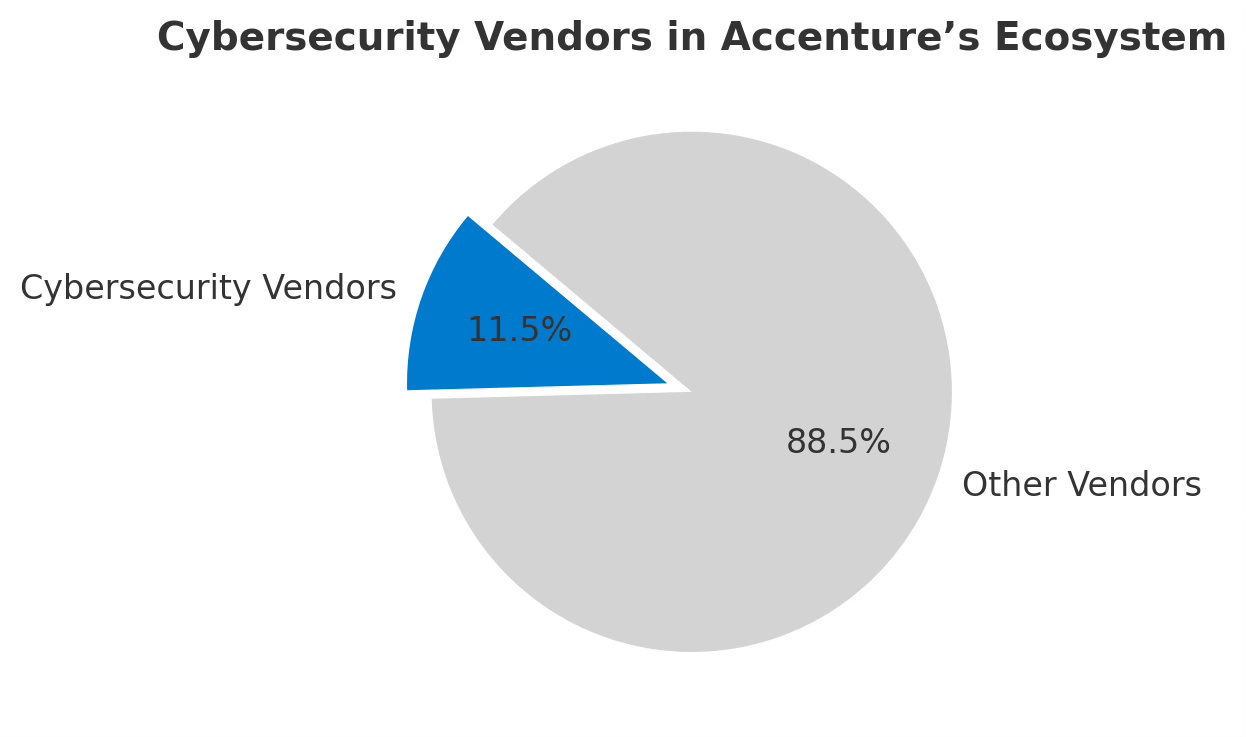

If we analyze one of them in detail (Accenture), we see that they have a broad partner ecosystem. The firm lists around 260 technology partners on its website, including approximately 30 dedicated to cybersecurity.

The majority of these partners are based in North America, with two from Israel and two from Europe. Each of these vendors typically generates at least several hundred million dollars in annual recurring revenue (ARR). Accenture has been named Partner of the Year 2025 in the Americas by Crowdstrike, for instance.

Through these partnerships, Accenture covers various security sectors, such as Training & Human Risk Management, Threat Intelligence / Security Operations, Network Security / SASE / Firewalls, SIEM / Threat Detection & Response, Cloud Security / Cloud-Native Application Protection Platforms (CNAPP), Identity & Access Management (IAM) / Identity Governance, and Endpoint Protection / Extended Detection & Response (EDR/XDR).

Distributors

Distributors like Ingram Micro and TD Sinnex, along with their network of channel partners, extend a vendor’s market reach by offering bundled solutions and managed services.

This model not only simplifies procurement for resellers and clients but also fosters recurring revenue streams. As the channel continues to evolve, distributors are becoming technical advisors and managed service providers themselves, enhancing the value delivered to both vendors and customers.

A strong example of distributor success in cybersecurity is SHI International’s partnership with CrowdStrike. The companies announced that SHI has sold over $1 billion worth of CrowdStrike’s cybersecurity products, making CrowdStrike the first pure-play SaaS security vendor to achieve this milestone through SHI. Notably, over 70% of this $1 billion was generated in just the last three years.

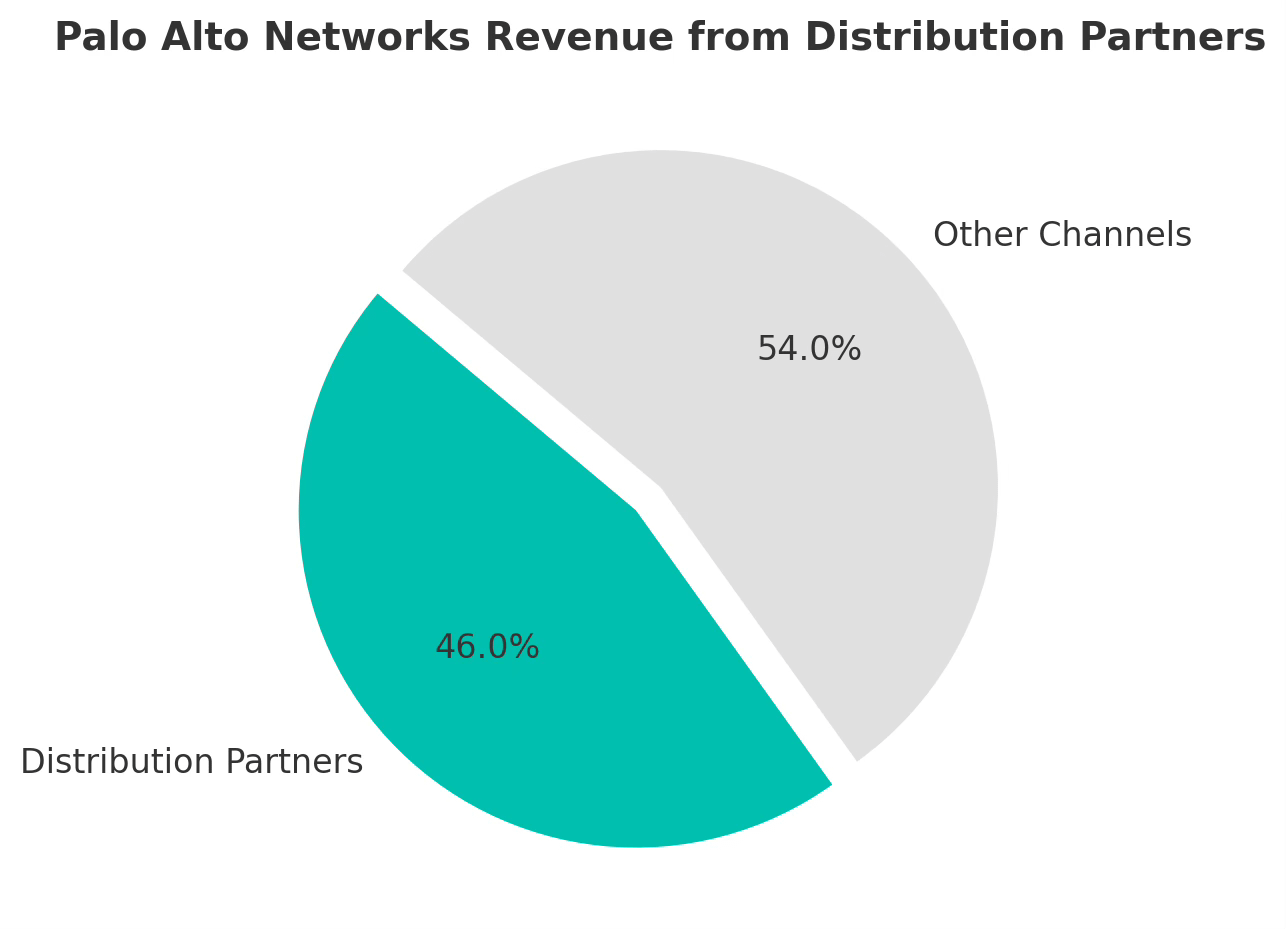

Palo Alto Networks, another multi-billion dollar cybersecurity vendor, also demonstrates the critical role of distributors, with three primary distribution partners accounting for approximately 45–47% of its total revenue.

Another example of this successful partnership between distributors and cybersecurity leaders: Fortinet relies almost entirely on distribution for its go-to-market model. In fact, a single distributor has accounted for roughly 28–31% of the company’s total revenue in recent years, according to their financial reports.

Cloud Marketplaces

Platforms such as AWS Marketplace, Microsoft Azure Marketplace, and Google Cloud Marketplace offer vendors immediate access to a global customer base. According to Canalys, enterprise software sales through these marketplaces are expected to grow from $16 billion in 2023 to $85 billion by 2028. By 2027, over 50% of hyperscaler marketplace sales are forecast to be driven via channel partners.

One of the primary drivers of cybersecurity software sales on marketplaces like AWS and Azure is the ability for customers to apply their committed cloud spend to third-party security solutions.

Enterprises frequently enter into large cloud commit contracts with providers like AWS, and purchasing security tools through the marketplace allows them to “burn down” those prepaid credits on critical solutions. This makes cloud marketplaces not just a procurement convenience, but a financial strategy.

CrowdStrike exemplifies the marketplace opportunity. In 2024, the company surpassed $1 billion in annual sales through AWS Marketplace alone. Transactions through AWS were, on average, four times larger than those via traditional channels and closed significantly faster.

With over 50 native integrations with AWS services and a strong partner ecosystem, CrowdStrike demonstrates how a strategic marketplace presence can be a game changer.

Other cybersecurity leaders are also thriving on cloud marketplaces. Splunk and Okta have each reached $1 billion in AWS Marketplace sales. Meanwhile, Wiz has revealed that 50–60% of its total revenue now flows through cloud marketplaces.

Besides AWS, Azure or Google Cloud, there are other type of marketplaces that are having a strong impact on the success of cybersecurity companies. One of them is Pax8, that we can classify as a cloud distributor.

Pax8 has created a purpose-built platform for MSPs and IT service providers to procure and manage SaaS solutions—including cybersecurity offerings—for SMB and mid-market clients.

Pax8’s marketplace surpassed $1 billion in ARR and reached $2 billion in total revenue within just 18 months. Security offerings are among the most “highly-utilized” products within the Pax8 ecosystem.

A recent Pax8 survey highlighted that over one-third of global IT solution providers now generate more than 20% of their revenue via marketplaces, with the highest engagement levels seen in North America and Europe. Being listed in Pax8 has now become a go-to-market strategy for many cybersecurity companies due to their rapid growth and reach.

Analyst Firms

Organizations like Gartner and Forrester wield significant influence through their evaluations and market analyses. Inclusion in Gartner’s Magic Quadrant or Forrester’s Wave reports can substantially boost a vendor’s credibility and visibility.

Gartner produces approximately 25 Magic Quadrants specifically focused on cybersecurity domains, while Forrester regularly publishes Wave reports covering areas such as incident response, risk ratings, and cybersecurity consulting.

These reports directly impact enterprise procurement decisions and vendor strategies not only for end customers but also for distribution channels.

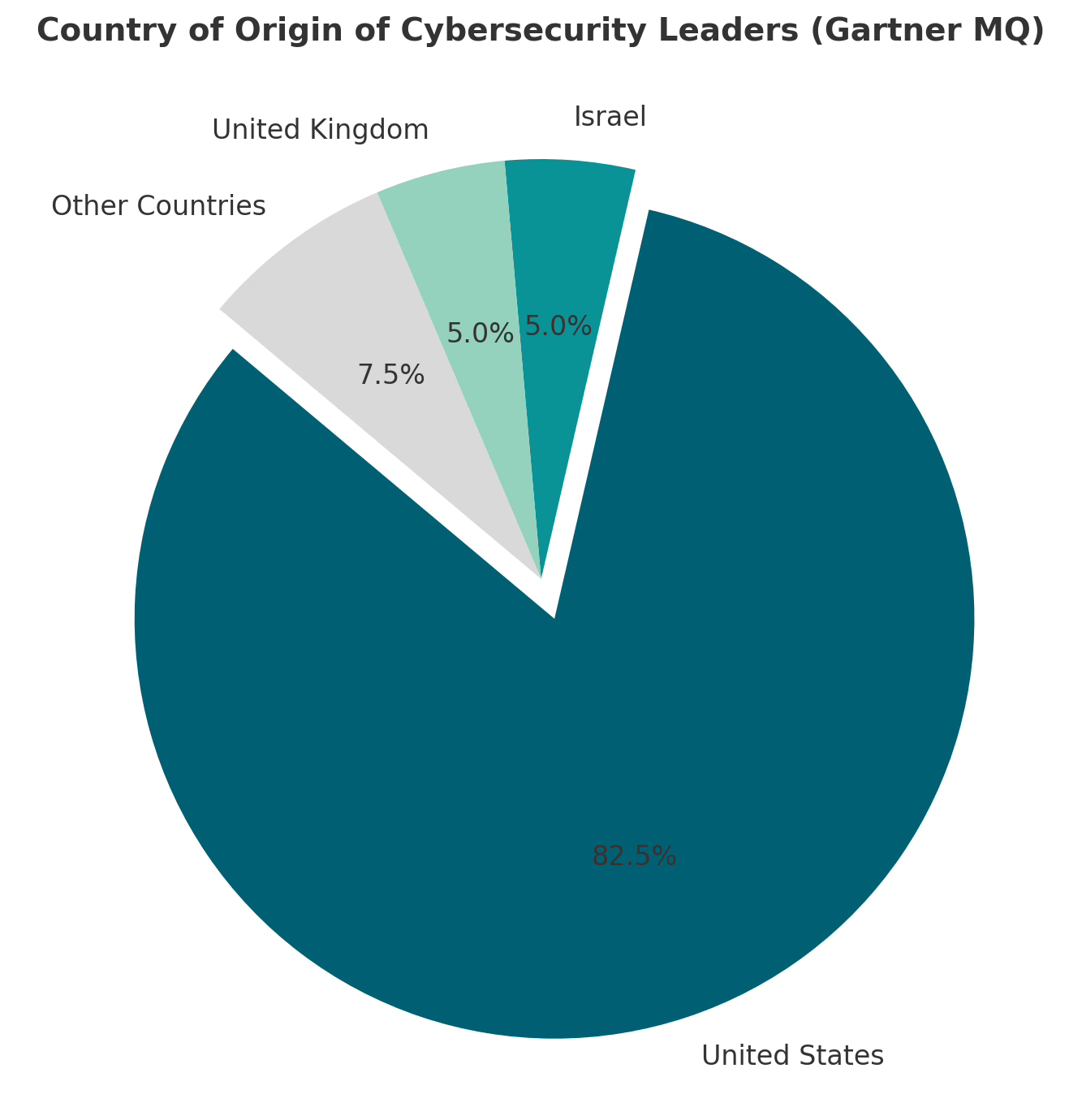

In the past, I made an analysis of the geographic distribution of the Gartner Magic Quadrant leaders, based on the analysis of 10 of those reports. Out of 40 leaders identified, 33 were based in North America, while only 2 each come from the UK and Israel. Notably, none are headquartered in the European Union.

This disparity highlights the dominance of North American vendors in gaining analyst recognition, which in turn reinforces their market leadership.

Magic Quadrants and Waves aren’t the only influential outcomes from the analyst firms that vendors seek. Cool Vendor status, Critical Capabilities research and more are badges that cybersecurity companies can use to create strong foundations for their growth strategies.

Consumer Cybersecurity Kingmakers

The consumer market for cybersecurity, while smaller, still has a lot of potential as I have already explored in a previous article. In my opinion, as more people work from home, there is a lot ahead in terms of security for individuals, and understanding who are the most influential companies is highly important.

Device Manufacturers

OEMs like Dell, HP, and Samsung play a critical role by pre-installing cybersecurity software on consumer devices. These partnerships enable vendors to reach users at the point of sale, often increasing adoption and stickiness.

For decades, Symantec’s Norton and McAfee dominated this space on Windows PCs, effectively leading the market by striking deals with almost every major computer manufacturer.

This channel made McAfee one of the kings in their space: a 2010 European Commission analysis noted that OEM pre-installs were a major channel, accounting for a large portion of consumer antivirus revenue for these companies.

In McAfee’s case, the OEM channel was the single largest source of its consumer segment revenue, with partners that included Acer, Dell, HP, Lenovo, Samsung, and Toshiba—essentially a who’s who of the PC market.

Symantec and Norton similarly leveraged these partnerships to become the two largest cybersecurity vendors in the space during the late 2000s. The vast majority of new Windows PCs came with one of the two pre-installed, creating a duopoly that was difficult for other vendors to penetrate.

Microsoft’s entry into the space with Windows Defender, starting with Windows 8 and continuing into Windows 10, disrupted the OEM channel by providing a built-in baseline antivirus to all users. However, during the 2000s, the OEM pre-install pipeline was arguably the single biggest factor in Symantec’s and McAfee’s global dominance.

Retail and E-tail Channels

Traditional retailers and online platforms like Amazon are key distribution partners for consumer cybersecurity solutions. Their expansive customer reach and marketing clout amplify product visibility and credibility.

A compelling historical example is Kaspersky, a Russian-founded security firm that broke into Western markets by aggressively expanding retail distribution. In 2002, Kaspersky partnered with MediaGold, a European business development firm, to boost its retail channel presence.

The goal was to place Kaspersky’s boxed antivirus products in “virtually all available retail sales channels” across key European countries. This push paid off, and over the next decade, Kaspersky became one of Europe’s most visible consumer security brands, often seen in electronics stores and PC shops.

By 2016, Kaspersky reported over 400 million users globally and held the largest market share of cybersecurity software in Europe. Retail visibility, from Media Markt in Germany to Dixon’s in the UK, made Kaspersky a household name and a default choice for consumers.

As sales shifted to digital, e-tail platforms like Amazon emerged as the new battleground. My own experience supports this transition: in markets where ESET had strong visibility and reviews on global e-tailers like Amazon, that exposure directly correlated with market leadership.

Telcos and ISPs

Telcos and ISPs are increasingly bundling cybersecurity services with broadband packages, providing vendors with access to massive customer bases. Omdia reports a growing trend among telcos to offer total consumer cybersecurity solutions, underscoring the channel’s strategic value.

One of the most prominent examples in this space is F-Secure, a Finland-based consumer cybersecurity vendor. Since the early 2000s, F-Secure has focused heavily on the operator channel and built what analysts refer to as “the largest telco operator network” in the cybersecurity industry. This early and strategic commitment to telco partnerships enabled F-Secure to scale its global presence and embed its solutions directly into consumer offerings from telecom providers.

McAfee is another major vendor that has leveraged telco relationships to expand its reach. For instance, McAfee partnered with British Telecom (BT) to power “BT Virus Protect,” a security suite offered free to all BT broadband subscribers. BT marketed this as “the most comprehensive free online security tools of any major UK broadband provider,” emphasizing its long-standing partnership with McAfee.

In Spain and Latin America, Telefónica adopted a “Security by Default” strategy with McAfee, rolling out McAfee-powered protection for all broadband and mobile customers under its Movistar brand. This included router-level protection and multi-device antivirus licensing, with Telefónica calling it the first instance of a telco delivering comprehensive cybersecurity to all customers regardless of connection type, immediately covering millions of users.

On the mobile front, Lookout offers a notable example. It became a leader in mobile security primarily through carrier preload deals. In 2012, T-Mobile began pre-installing Lookout Mobile Security on all Android devices it sold. By 2013, this rollout expanded to most T-Mobile Android handsets, and similar agreements were formed with AT&T and Sprint.

A major milestone came in 2013 when Lookout partnered with Samsung to embed its software into the Samsung Knox security suite, gaining global reach as the app came pre-installed on all Knox-enabled devices. This dramatically expanded Lookout’s user base, and by 2014, the company reported over 50 million users worldwide.

Another notable player in this channel is Whalebone, a European cybersecurity firm that has built its presence almost entirely by focusing on telecom operators. The company’s growth highlights how telco partnerships can provide a robust foundation for scaling cybersecurity offerings to mass markets.

Other Kingmakers

There are other entities that could be considered relevant in the making of a cybersecurity leader. For instance, in the consumer market, magazine reviews play a significant role, where becoming a leader in one of their comparatives can have a direct impact on the sales of a company.

Many European companies, for instance, work closely with their local governments at the beginning of their journey, which helps them to reach a significant position in their home markets.

While this can be a strong initial boost, it can also be a blocker. Public sector contracts can provide early-stage support and market legitimacy, but they have a limited reach, as they are only influential within their country.

On the other hand, regulations, procurement processes and local requirements can easily transform this into a disadvantage, where vendors need to dedicate too much time and effort to maintain their local position instead of being able to develop further globally.

Other relevant drivers of success are the initial investors in the cybersecurity vendors. They can provide expert guidance and support during the early days, and more importantly, they can enable their portfolio companies through introductions to, for instance, the above kingmakers.

If a cybersecurity startup counts in their board with people that can open the door to Global System Integrators or Distributors, that can put them on the path to success.

The Strategy of Success

Growing a cybersecurity company takes time, dedication and effort, and most importantly, a winning strategy. Understanding who are the channels or partners that can accelerate the growth of a vendor is key to develop the right approach to the market early on.

The decisions that cybersecurity startups make in their first steps will influence their future, as even partnering with the right investors will have an enormous impact.

Companies can have the best and most disruptive technology and solution, but if they don’t find their way to the kingmakers, they will need to work harder to achieve lower results than those that are currently the leaders in the market.

The above data and insights clearly show what is the reach and coverage that those entities have, and moreover, they play another important role besides being kingmakers: they are also gatekeepers.

While the Customer is the ultimate-decision maker, the kingmakers exert a strong influence on them. The decisions of Enterprise CISOs, IT buyers and consumers alike are heavily shaped by the endorsements, partnerships and integrations provided by system integrators, distribution partners, analyst firms and the rest.

The customer decides, yes, but from the choices that are known to them, and in many cases, those are limited to the options provided by the organizations that they already have relationships with.

For instance, when a customer already made the decision of working with a particular GSI, they have limited their options to those within their portfolio, and that is the power these organizations have.

Knowing what is the impact of the kingmakers in the cybersecurity market helps vendors, from startups to established ones, to develop the right strategy for them and truly become the leaders in their sectors.

*** This is a Security Bloggers Network syndicated blog from Cybersecurity & Business authored by Ignacio Sbampato. Read the original post at: https://cybersecandbiz.substack.com/p/kingmakers-in-cybersecurity