Credit Card Tokenization: Everything You Need to Know

As the progress of payment technology gathers pace, the potential threat to sensitive customer data increases at a similar speed. A particular danger arises with the storing of customer payment details, and it is therefore vital that organizations take appropriate measures to heighten data security and prevent credit card fraud.

If your organization accepts credit card payments, tokenization is one of the most secure ways to protect against loss or theft of customer information. But what exactly is credit card tokenization, how does it work, and what are the benefits?

What is Tokenization?

Tokenization is a data security feature where a sensitive data element or set is effectively replaced (“tokenized”) with a non-sensitive alternative, called a token. This renders the data completely useless to exploitation.

Tokenization can be used to safeguard data in a number of areas such as medical records, banking and credit card payments. In other words, is it possible to tokenize credit cards – let’s see, how.

What is credit card tokenization?

Credit Card tokenization is the process of replacing sensitive customer details with an algorithmically generated number that is impossible to trace back to the original data or information. The result – a (credit card) token – makes it impossible for anybody to misuse sensitive information, as the tokenization algorithm ensures that the data is unable to be traced back to its original source.

As an example, when a customer makes a purchase using a credit or debit card, the tokenization process takes the card number and transforms it into a mathematically irreversible token. If the credit card number or account number needs to be billed again in the future (such as for a recurring payment or subscription), the payment system recognizes the token associated with the card, rather than the card number itself.

Credit or debit card tokenization increases trust for organizations and significantly reduces the risk of sensitive data such as cardholder data being exposed.

How does credit card tokenization work?

The tokenization process can take many forms, but it’s useful to consider the following possible scenarios:

1. Ecommerce Payment Tokenization

- A customer makes a purchase and uses their credit card to check out (e.g. 1923 1242 4629 2649).

- The card number is changed to a random sequence of characters (e.g. EUSH127ABD5562).

- The relationship between the actual card number and the token is stored in a separate vault.

- If the transaction is recurring (for example, for a monthly subscription) or a refund is required, the merchant can simply use the token rather than needing to store the sensitive card data itself.

2. Mobile Payment Tokenization

When users of Apple Pay or Android Pay add a credit card to their mobile device, each of the card numbers will be tokenized and stored on the phone. When a purchase is made, the token is used instead of the payment card itself, thus adding an extra layer of protection for the transaction.

3. App Payment Tokenization

Using applications to purchase goods is becoming more common (groceries, clothing etc). If your phone contains a token, these apps are unable to retrieve or access any credit card details. All bank details are locked down and hackers/fraudsters would be unable to commit an offense with the data available to them. Checking out to finalize a purchase is simple too as many apps are integrated to be linked directly with your stored shipping and billing information.

What are the benefits of credit card tokenization?

The decrease in data theft and fraud as a result of tokenization means businesses are less likely to incur reputational or financial damage as a result of a data breach. Customers will also feel reassured and confident in shopping with merchants who utilize a tokenization process, as this shows a strong emphasis on protecting the sensitive information of the customer.

Tokenization also has additional benefits, particularly when combined with PCI-validated Point-to-Point Encryption. As well as ensuring unsecured payment data never enters your organization’s systems and safeguarding against cybersecurity threats, tokenization helps with PCI compliance and reduces the scope of PCI-DSS audits, saving both cost and time.

Tokenization Vs. Encryption

If you’re familiar with tokenization, you may have also heard of credit card encryption. How is tokenization different from encryption?

When data is encrypted, it is coded into a hidden language, similar to tokenization. However, encryption uses a mathematical formula which is possible to reverse-engineer, meaning encrypted sequences can be deciphered and risks exposing sensitive information such as credit card data.

Conversely, tokenization turns a meaningful piece of data into a string of random characters that cannot be reversed – so if breached, no meaningful value is exposed. This is a huge benefit in the payment card industry, ensuring the highest security standard possible. The only thing a hacker would obtain is a list of token numbers which would be of no use to them. This makes credit card data unusable, adding additional layers of security.

Tokenization & Encryption FAQ

Let’s take a closer look at tokenization and encryption through the most frequently asked questions.

What is Encryption?

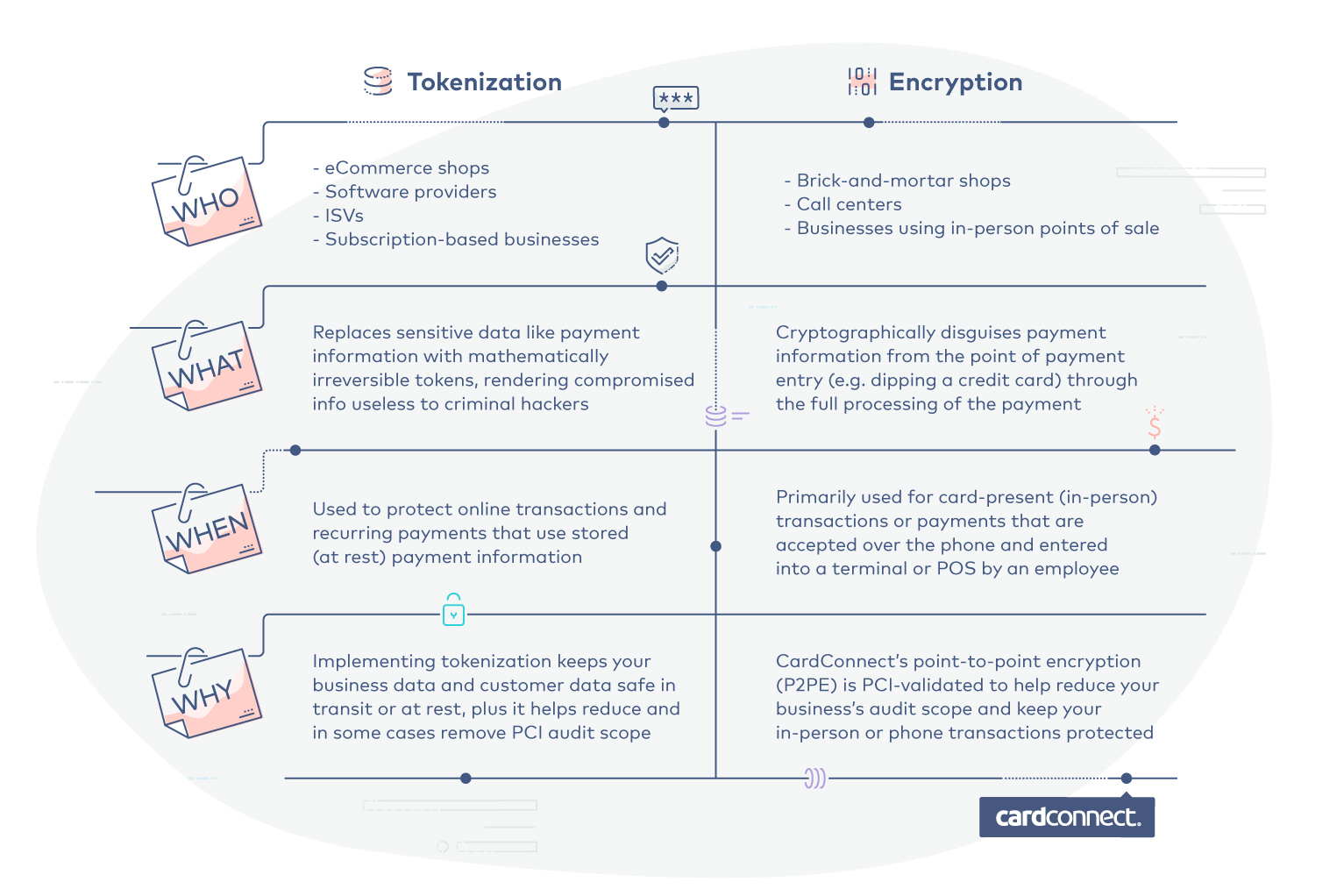

Cryptographically disguises payment information from point of payment entry (e.g. dipping a credit card) through the full processing of the payment.

Who Uses Encryption?

Brick-and-mortar shops, call centers, businesses using in-person points of sale.

Who Uses Tokenization?

Ecommerce shops, software providers, ISVs, subscription-based businesses.

When is Encryption Used?

Primarily used for card-present (in-person) transactions or payments that are accepted over the phone and entered into a terminal or POS by an employee.

When is Tokenization Used?

Used to protect online transactions and recurring payments that use stored (at rest) payment information.

Why is Encryption Used?

CardConnect’s point-to-point encryption (P2PE), as an example, is PCI-validated to help reduce your business’s audit scope and keep your in-person or phone transactions protected.

Why is Tokenization Used?

Implementing Tokenization keeps your business data and customer data safe in transit or at rest, plus it helps reduce, and in some cases remove PCI audit scope.

To learn more about how CardConnect utilizes both tokenization and encryption to ensure maximum security, fill out the form below and we’ll connect you with our support teams.

*** This is a Security Bloggers Network syndicated blog from LaunchPointe: Payment Security authored by CardConnect. Read the original post at: http://feedproxy.google.com/~r/Launchpointe-PaymentSecurity/~3/quCDtB46l6M/tokenization-101