Hit or Miss

One of the main obstacles against adopting a quantitative approach to

risk management is that since major security breaches are relatively

rare and hence, there cannot be enough data for proper statistical

analysis. While this might be true in the classical sense, it is not if

we adopt a Bayesian mindset, which basically

amounts to being open to change your beliefs due to new evidence.

Remember the Rule of 5? It allows us to give a

90% confidence interval with only 5 samples. This is already a

counterexample for the “not enough data” obstacle. Also recall how we

used probability distributions in order

to run simulations on many possible scenarios and updated our beliefs

based upon evidence, all based only on a few expertly estimated

probabilities. In this article we will show how a probability

distribution can be derived from simple observations.

Suppose we want to estimate the batting average –the ratio of hits to

the number of times he stands at the bat– for a particular player. One

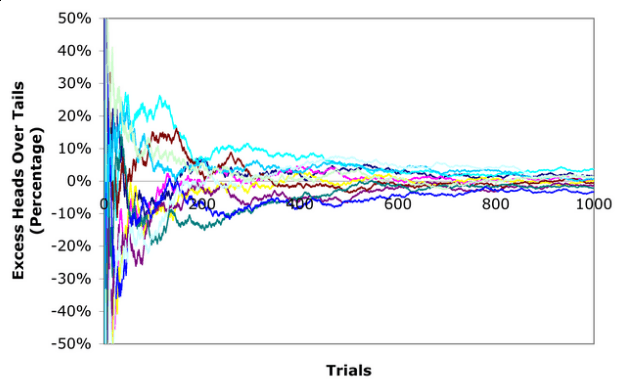

way to do so would be to look at their rolling

average, i.e., his

average so far. The law of large

numbers tells us

that no matter what happens at the beginning, the rolling average will

tend to the true value, if you observe it for long enough:

Figure 1. Rolling average tends to the true mean. Via

Brad DeLong.

The only problem is, we don’t have long enough. Baseball seasons are

finite, and major cybersecurity events are few and far between. What is

one to do? If we go with the rolling average like in the above image, we

would be stuck with the initial, imprecise part of it. For instance,

after the first try, the player’s average will be either exactly 0 or 1,

which clearly does not reflect the reality well.

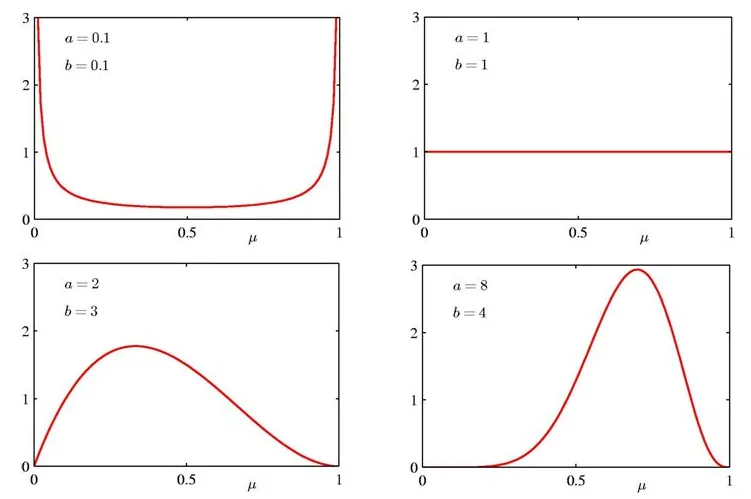

Enter the beta probability distribution. This distribution takes two

parameters which determine its shape and spread, and are cryptically

called alpha and beta, but in reality can be though of as hits and

misses from a certain sample. We may also think that the density

function of this distribution gives us the probability that a

proportion, ratio or probability of an event is just that. No, it

was not a typo. We can think of the beta distribution as being the

probability distribution of probabilities themselves. As such, we can

use it to obtain the probability of being attacked after having observed

who has been attacked (the hits) and who has not (the misses) in a

certain period of time.

Figure 2. Beta distribution with different parameters.

By Shona Shields on Slideplayer.

Wait: it gets better. The beta distribution can be updated with evidence

and observations, just like we did when working with Bayes

Rule, to give better estimations. Since alpha and

beta represent hits and misses, and if we observe some breaches and some

non-breaches, why not just add them to the original parameters?

It can be shown that the beta distribution, modified this way, reflects

reality much better than the previous estimate. And we can continue

doing this in a repetitive manner everytime there is an observation.

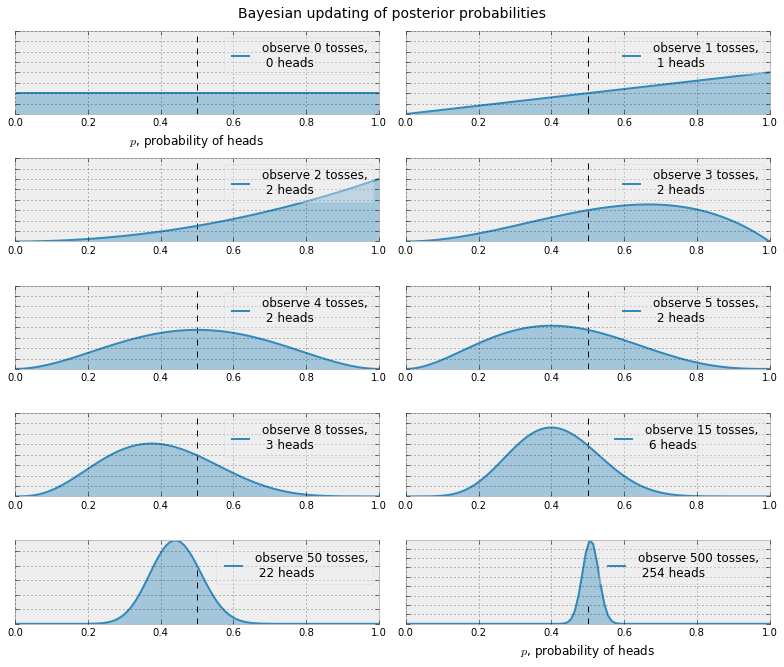

Imagine an even simpler situation: what is the probability that a coin

lands heads? We don’t know whether the coin is fair or has been loaded

to give more priority to some results than others, so we might just roll

it many times, record the results (how many heads and how many tails)

and fit a beta distribution in the manner described above. The results

would be as follows:

Figure 3. Adjusting a beta distribution to new evidence[1]

Notice how the distributions after the first two tosses resulted in head

do not just say that the probability of heads is 100%, which is what the

rolling average would point to, which is clearly wrong. Instead, the

beta distribution sort of smoothes out what would be a sharp, extreme

yes/no situation, allowing a chance to values in between. After only 3

tosses the distribution starts to look like a proper distribution. It

gives the probability that the probability of obtaining heads has a

certain value. After 50 tosses we can conclude, with evidence and a

mathematically sound supporting method, that the coin was fair after

all.

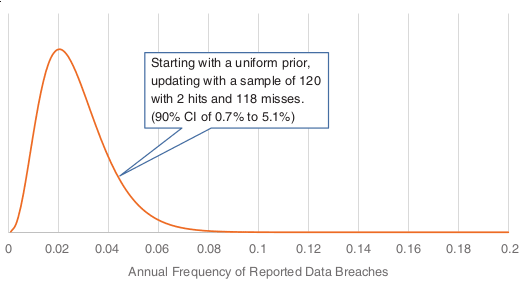

Next, how do we go about applying this to security breaches? What

exactly would be the “hits” and the “misses”? Recall that we update

our knowledge of hits and misses by taking random (tough typically

small) samples from an unknown, allegedly large population. Since we

want to estimate the probability that a business like our own would

suffer a major attack, then the population should be a list of companies

similar to ours. Call that the top 10, 100, etc of your

country/region/world. Out of those, take a random sample, and check

against a public database of cybersecurity events (such as the Verizon

Data Breach Investigations

Report) to see

if any of the sampled companies suffered an attack.

We also need seeds for the alpha and beta parameters. These could be

expert estimations or, if you want to be very conservative, you can set

both to 1, which would give simply a uniform distribution (everything is

equally likely). This is the most uninformative of all possible

priors. It is totally unbiased. Again, by the law of large numbers, it

doesn’t really matter much where we begin. But the better the initial

estimates, the faster the convergence to the “truth”. Starting with this

uniform prior and observing that there is one attacked company in the

sample over a 2-year period, we obtain the following beta distribution:

Figure 4. Beta distribution for breach frequency.[2]

When we have a distribution, we know pretty much everything. We can give

find an expected probability of attack or, better yet, a 90% confidence

interval in which that probability lies. We can also use it to update

our previous models. Remember that in our

simulations to obtain the Loss

Exceedance Curve, we used a log-normal distribution simply because it

was the best fit due to some of its properties. Now we have a better

reason to use this beta distribution we obtained here, and running the

simulations again with this distribution would yield the following

results:

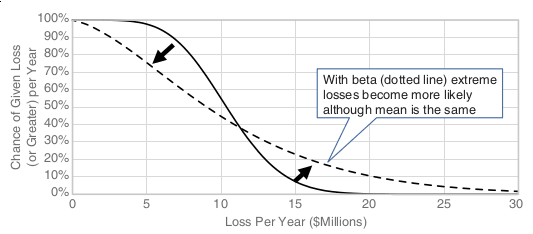

Figure 5. Updated LEC

Notice how, by using the beta distribution, it is clear that higher

losses are more likely, while smaller losses are less so. Given that

this beta distribution was built using real data, this should be a more

appropriate estimate of reality.

Thus, the Bayesian interpretation of statistics and, in particular, the

iterative updating of a fitted beta distribution can aid your company in

better understanding risk, and not only in cibersecurity, since nothing

in this method is inherent to cybersecurity risk. Especially in

combination with random simulations,

which turn these abstract distributions into concrete bills and coins.

References

C. Davidson-Pilon (2019). Probabilistic Programming and Bayesian

Methods for

Hackers.D. Hubbard, R. Seiersen (2016). How to measure anything in

cibersecurity risk. Wiley.M. Richey M. and P. Zorn (2005). Basketball, Beta, and

Bayes. Mathematics

Magazine, 78(5), 354.D. Robinson (2015). Understanding the beta distribution (using

baseball statistics). Variance

Explained.

*** This is a Security Bloggers Network syndicated blog from Fluid Attacks RSS Feed authored by Rafael Ballestas. Read the original post at: https://fluidattacks.com/blog/hit-miss/